SOFR Interest Rate Update - Late Jan/Early Feb

February 8, 2024

On December 31st, the US Federal Reserve (the Fed) completed their first meeting of 2024. In a widely anticipated move, they decided to hold US Federal Funds Rates (Fed Rates) steady. This makes for a fourth straight meeting holding rates steady, dating back to July 2023.1 Fed Chair Jerome Powell built upon his comments following the Fed’s December meeting, indicating the Fed is no longer concerned they’ll need additional rate hikes but that their focus is on the timing of when to start cutting rates.2

Markets continue to be optimistic that rate hikes are around the corner, prompting Powell to address the speculation about when Fed would start cutting rates, stating “I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting [to justify a rate cut]” in his post-meeting press conference.2 Both Powell and the Fed’s official statement reiterated their intention to closely monitor inflation data and the economic outlook and that “the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably towards two percent.”1

Reading between the lines, it appears the Fed governors are still focused on balancing the risks between cutting rates too fast (and risk increasing inflation again) and too slow (and potentially jeopardizing the “soft landing” they are trying to accomplish for the US economy). Following their meeting, markets have adjusted and we’ve updated our borrowing rate assumptions to reflect the current market outlook. Below are charts and additional analysis showing forward rate projections and key items of interest to monitor between now and our next update.

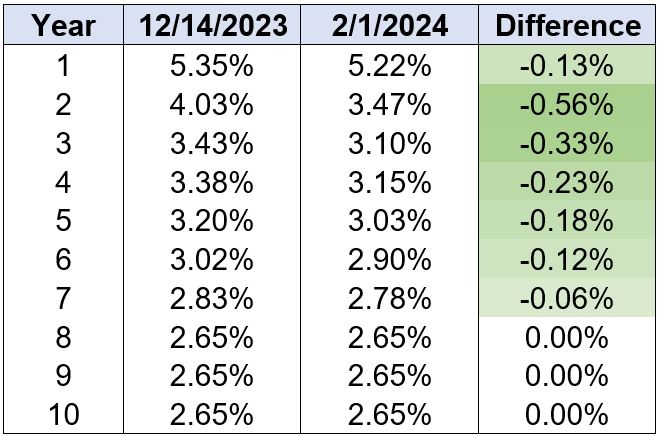

Chart 1 below compares our current Secure Overnight Financing Rate (SOFR) projections to our projections from our December 14th update. These rates are based on the most-current Fed Dot Plot and the SOFR Forward Curves on each date shown. Forward rate assumptions have dropped as both The Fed and markets continue to see signs of slowing inflation.

Chart 1

Year 1 - 7 Average: -0.23% | Year 1 - 10 Average: -0.16% | Data derived from Forward SOFR Curve provided by Pensford and Fed Dot Plot Data. This data fluctuates daily, and what is depicted above is as of 2/1/2024.

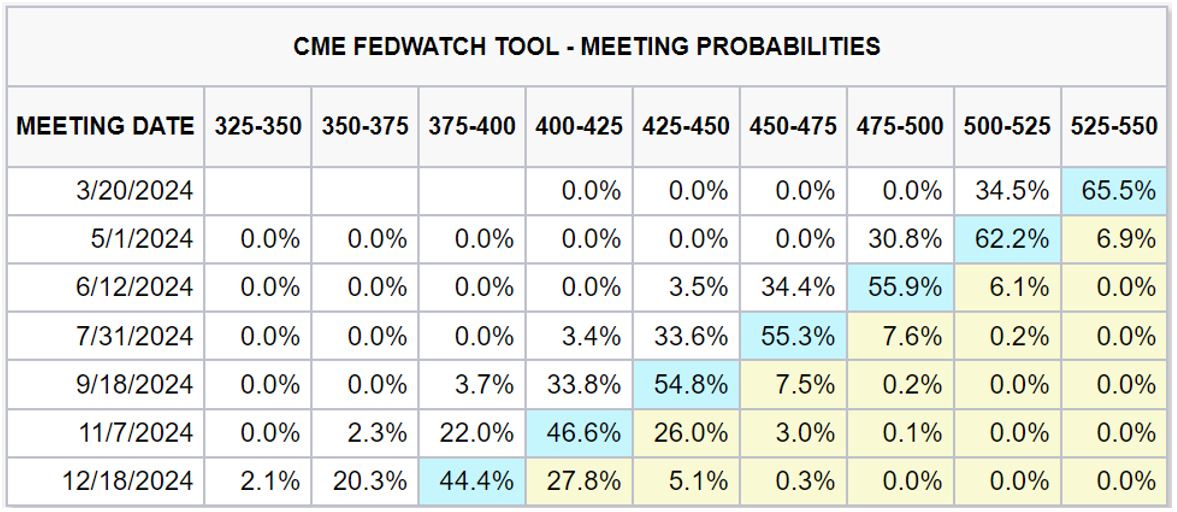

Markets are currently projecting there will be more rate cuts than the three the Fed had baked into their December 2023 projections.1 Chart 2 below shows CME Group’s Probabilities for Fed Rates for each meeting this year. As of February 1st, they’re projecting a 94.6% probability of at least four rate cuts and 66.8% probability of at least six before the end of 2024. The Fed’s updated Dot Plot following their March meeting should provide immense insight as to how their projections have changed since December.

Chart 2

This data fluctuates daily, and the data depicted above is as of 2/1/2024.

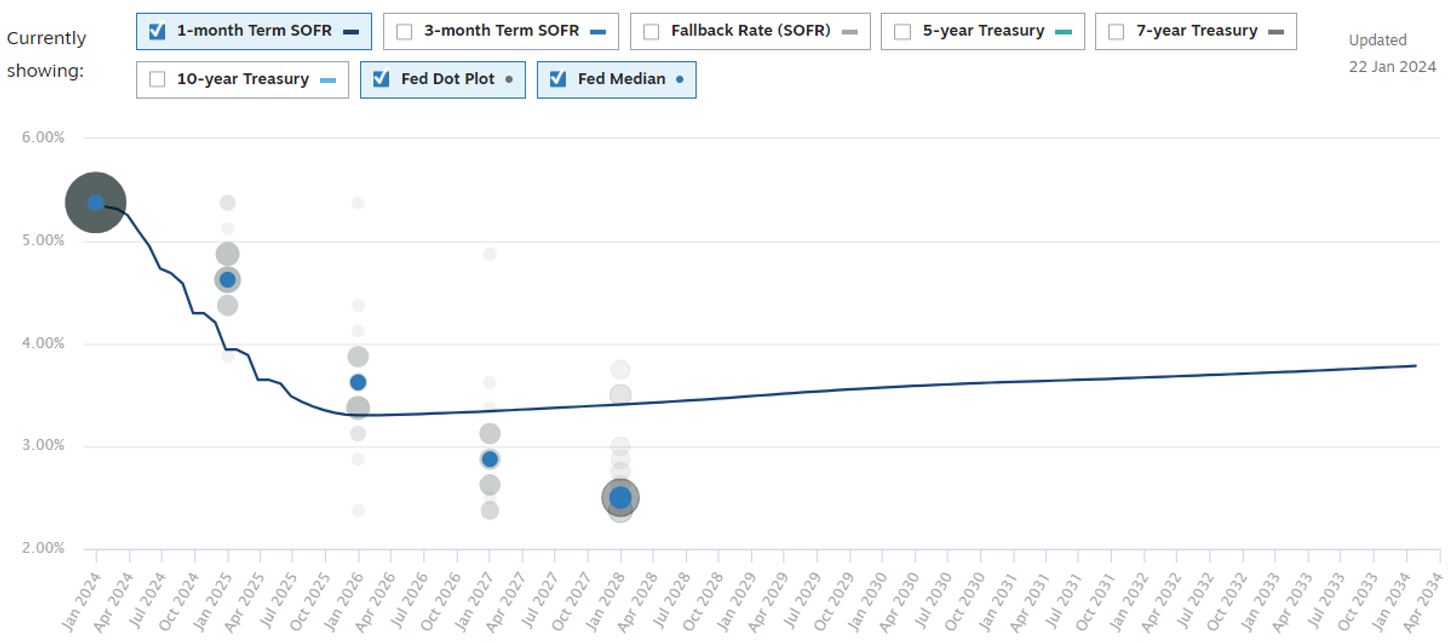

Chart 3 compares the Fed’s December Dot Plot (gray dots) and Median (blue dots) to the current SOFR forward projections (blue line). Similar to Chart 1, forward assumptions have dropped slightly in the last six weeks, but haven’t changed dramatically.

Chart 3

This data fluctuates daily, and what is depicted above is as of 2/1/2024.

With a contentious presidential election cycle on the docket for 2024, Fed officials are already beginning to come under fire by politicians on both sides of the aisle and well aware that will only ramp up throughout the year. The Fed is trying to take a proactive approach to reiterating their independence from partisan politics, with Powell dismissing politics as a potential influence on the Fed in his most recent press conference and Esther George, former Kansas City Fed president, explicitly stating “it [politics] doesn’t influence the discussions” last month. Still, the Fed has to be especially careful in how it communicates decisions this year.

Ultimately, rates continue to trend lower and market projections indicate that the US is heading towards monetary easing in the near future. Exactly how soon cuts begin and how quickly they drop is the biggest question mark. While the Fed’s March meeting feels unlikely to be accompanied by a rate cut, the Fed could be pushed to act sooner than expected if the US economy shows signs of slowing.

As mentioned in previous updates, the average time between the first rate hike and cut since 1993 has been 2.2 years. Since the Fed’s first rate hike of this cycle was in March 2022 , the average would take us exactly to The Fed’s May 2024 meeting. In the meantime, we will continue to monitor both inflation and economic activity to see how it impacts forward rate projections.

Schechter constantly monitors interest rates and updates our rate projections for our Premium Finance designs a minimum of once per month and following every Fed meeting. We will update additionally as needed based on the markets and various influencing factors. If you have any questions or would like to discuss interest rates or any other ongoing economic developments, please reach out to our team to schedule a call.

Contact Us to Schedule a Free Consultation

Sources:

https://www.federalreserve.gov/monetarypolicy/files/monetary20240131a1.pdf

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20231213.pdf

https://www.pensford.com/industry-news/the-feds-on-the-clock

https://fred.stlouisfed.org/series/FEDFUNDS