SOFR Interest Rate Update - Late March/Early April

March 25, 2024

On March 20th, the US Federal Reserve (the Fed) completed their second meeting of 2024, holding US Federal Funds Rates (Fed Rates) steady for a fifth straight meeting since their last rate hike in July 2023.1 Fed Chair Jerome Powell continued to build on his comments from the last few months, highlighting that “we believe that our policy rate is likely at its peak for this tightening cycle, and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year” while also doubling down on the Fed’s “wait and see” plan by noting they’re “prepared to maintain the current target range of the federal funds rate for longer, if appropriate.”2

While the Fed’s rate announcement and Powell’s comments were widely anticipated, there was much more uncertainty surrounding the Fed Dot Plot, which was largely unchanged and still projects three rate cuts this year.3 This was received positively by analysts and markets, after two months of higher-than-expected inflation data had many worried the Fed would project fewer rate cuts in 2024.4

Following their meeting, markets have adjusted and we’ve updated our borrowing rate assumptions to reflect the current outlook. Below are charts and additional analysis showing forward rate projections and key items of interest to monitor between now and our next update.

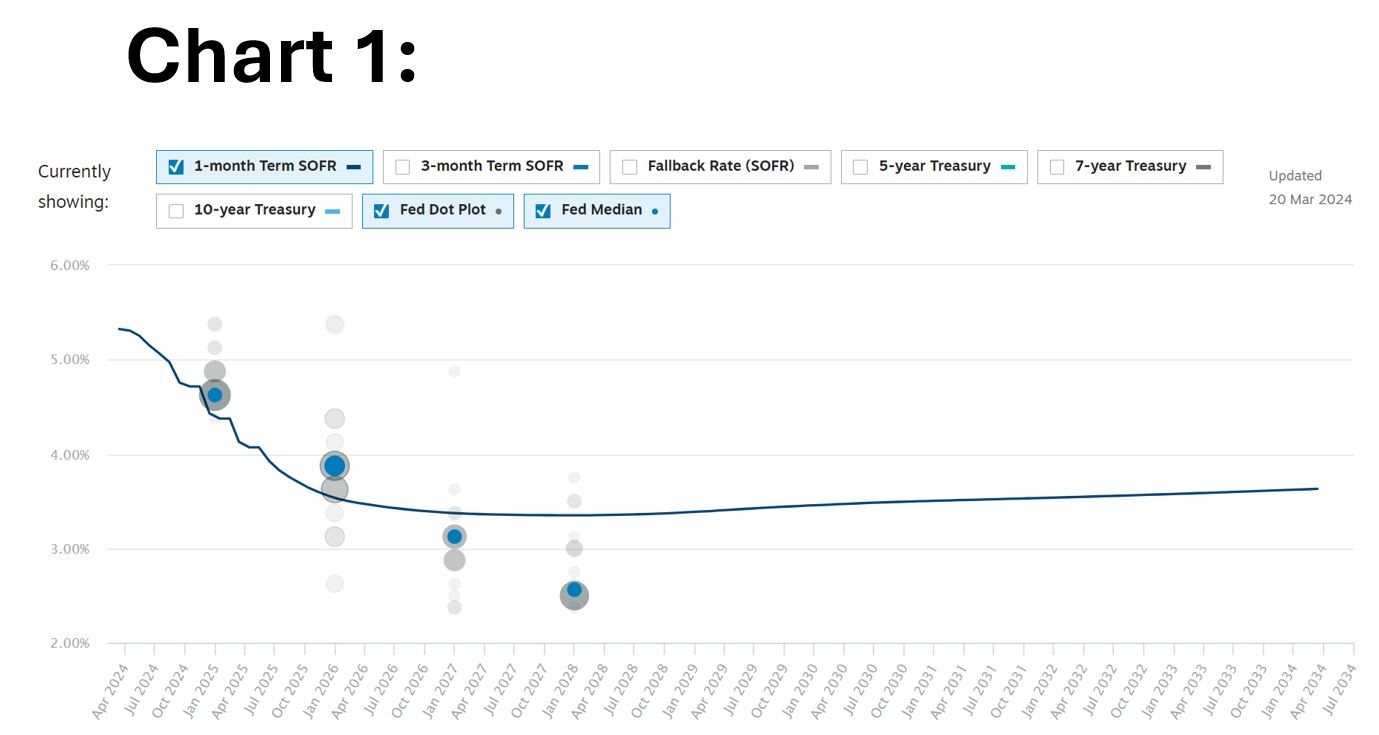

Chart 1 compares the Fed’s new Dot Plot (gray dots) and median (blue dots) to the current SOFR forward projections (blue line). Ultimately, this chart has not changed dramatically since our last update on 2/1. The Fed is still projecting three rate cuts in 2024 and while the Dot Plot median for 2025, 2026, and Longer Run are all up, it’s by an average of less than 10bps. The SOFR Forward Curve projects rates to fall slightly faster than the Fed in 2024 and 2025 but slightly slower thereafter.

This data fluctuates daily, and what is depicted above is as of 3/21/2024.

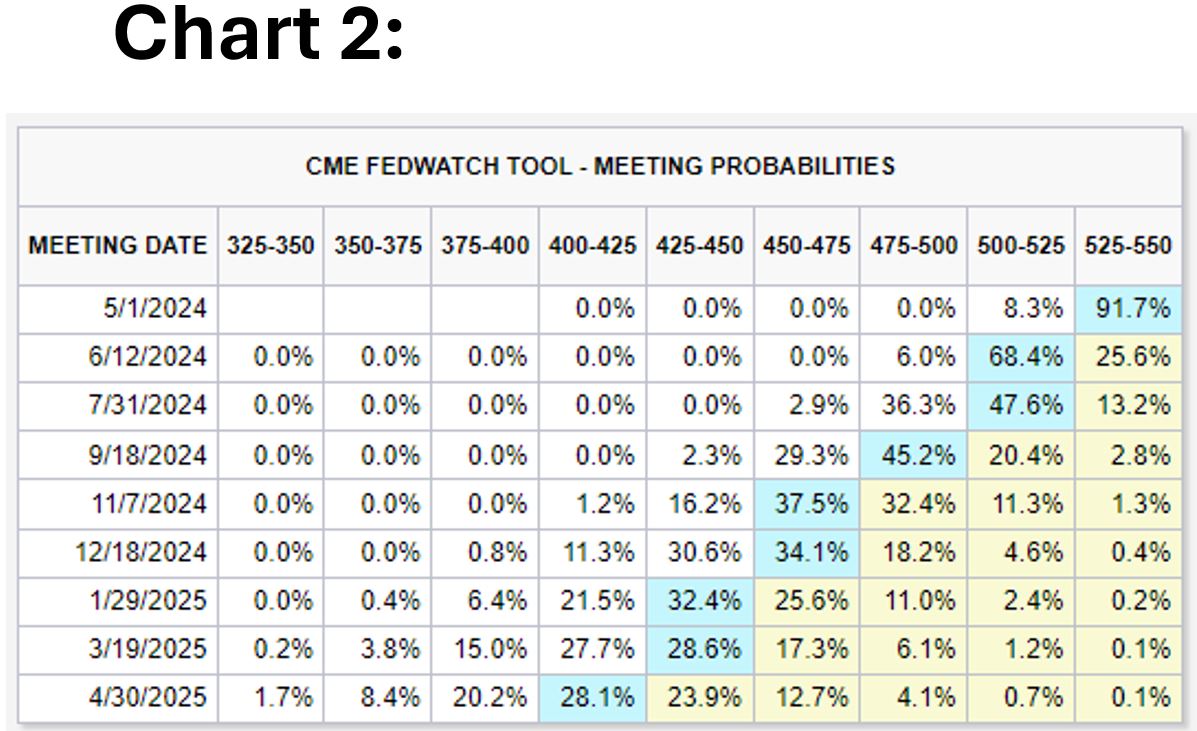

Those projections are supported in Chart 2, which shows CME Group’s Probabilities for Fed Rates for each meeting this year. As of March 21st, they’re projecting we’ll most likely see the first rate cut in June, with markets projecting three total cuts this year (in line with the Fed) and five total over the next 12 months. While markets still view a real possibility of more than three rate cuts in 2024, their current probability of 42.7% is dramatically lower than the 94.6% odds at the time of our last update. It’s also worth noting that while rates have historically moved faster than projections, more governors voted for less than three rate cuts before the end of the year than voted for more than three.

This data fluctuates daily, and what is depicted above is as of 3/21/2024.

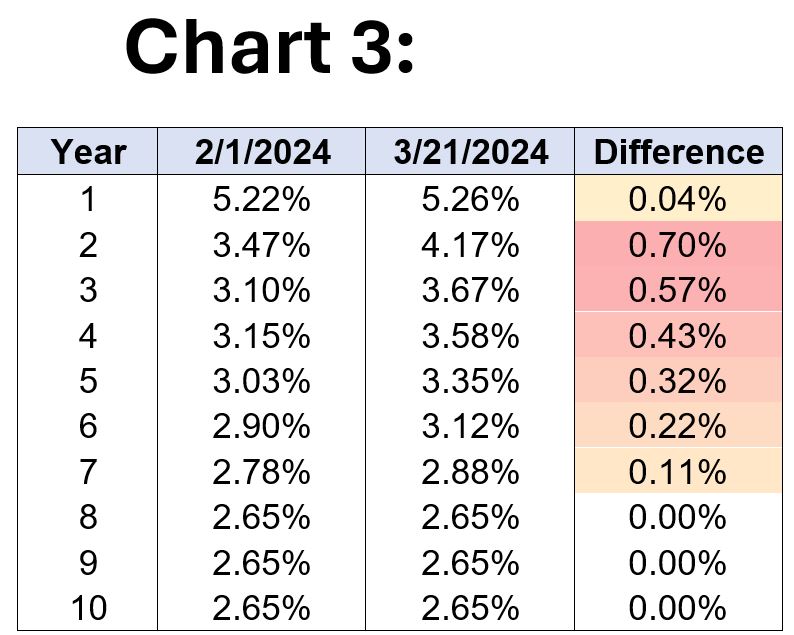

Finally, Chart 3 below compares our current Secure Overnight Financing Rate (SOFR) projections to our projections from our February 1st update. These rates are based on the most-current Fed Dot Plot and the SOFR Forward Curves on each date shown. While rates have crept up since our last update, they have held fairly steady over the last month or so and are still projecting relevant rate cuts over the next couple of years.

Y1-7 Average Difference: 0.34% | Y1-10 Average Difference: 0.24%

In hindsight, it appears that markets overreacted to the Fed’s positive commentary in December, due to better-than-expected inflation data in the month before and after it. When that was followed by two months of worse-than-expected inflation data, many investors assumed the Fed would hold rates higher for longer, and forward assumptions briefly overcorrected in the other direction. Meanwhile, the Fed’s commentary and analysis following their March meeting tells us the last three months haven’t changed their outlook, as noted by Powell when he said “we’re not going to overreact… to these two months of data, nor are we going to ignore them.”2

Powell further stated the January and February data “haven’t really changed the overall story, which is that inflation is moving down gradually on a sometimes-bumpy road towards two percent”2, which ultimately highlights what the Fed has been saying for months: they continue to be in “wait and see” mode and seem to be perfectly content to leave rates at their current plateau until changes in inflation, unemployment, or the economy give a compelling reason to move them. In the meantime, we will continue to monitor both inflation and economic activity to see how it impacts forward rate projections.

Schechter constantly monitors interest rates and updates our rate projections for our Premium Finance designs a minimum of once per month and following every Fed meeting. We will update additionally as needed based on the markets and various influencing factors. If you have any questions or would like to discuss interest rates or any other ongoing economic developments, please reach out to our team to schedule a call.

Sources:

1https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

3https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20240320.pdf

https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm